The Outlook for U.S. Nuclear Power

February 01, 2017

The U.S. nuclear power industry faces an uncertain future. While nuclear has held its 18-20% share of U.S. electricity generation, the total number of nuclear reactors/plants has fallen to 99, down from 104 in 2013. New nuclear development in the U.S. has long faced a variety of headwinds: high regulatory hurdles, spiraling costs, an aging workforce, a lack of waste storage facilities, and public apprehension.

In fact, even the states with the most ambitious climate goals have been prematurely shutting down nuclear power plants, very telling of the industry’s plight because nuclear is often classified as “zero-emission.” In California, the 2,100 MW San Onofre Nuclear Generating Station was shuttered in 2012, with the 2,160 MW Diablo Canyon nuclear plant set to be phased out by 2025. In New York, Governor Andrew Cuomo recently announced plans to close the 2,000 MW Indian Point nuclear plant, which supplies electricity to New York City and surrounding areas, by 2021 – more than a decade ahead of schedule.

Yet, advocates still hold out hope for the long-awaited “nuclear renaissance.” After all, nuclear power is carbon-free and supplies 65% of our “clean energy,” i.e., energy that does not come from fossil fuels. Some states, such as Illinois, have thrown a lifeline to nuclear by subsidizing struggling plants. Down south, as the largest public power company in the country, TVA’s Watts Bar 2 just became the first new commercial U.S. reactor of the 21st century. Four reactors are under construction at two sites in Georgia and South Carolina.

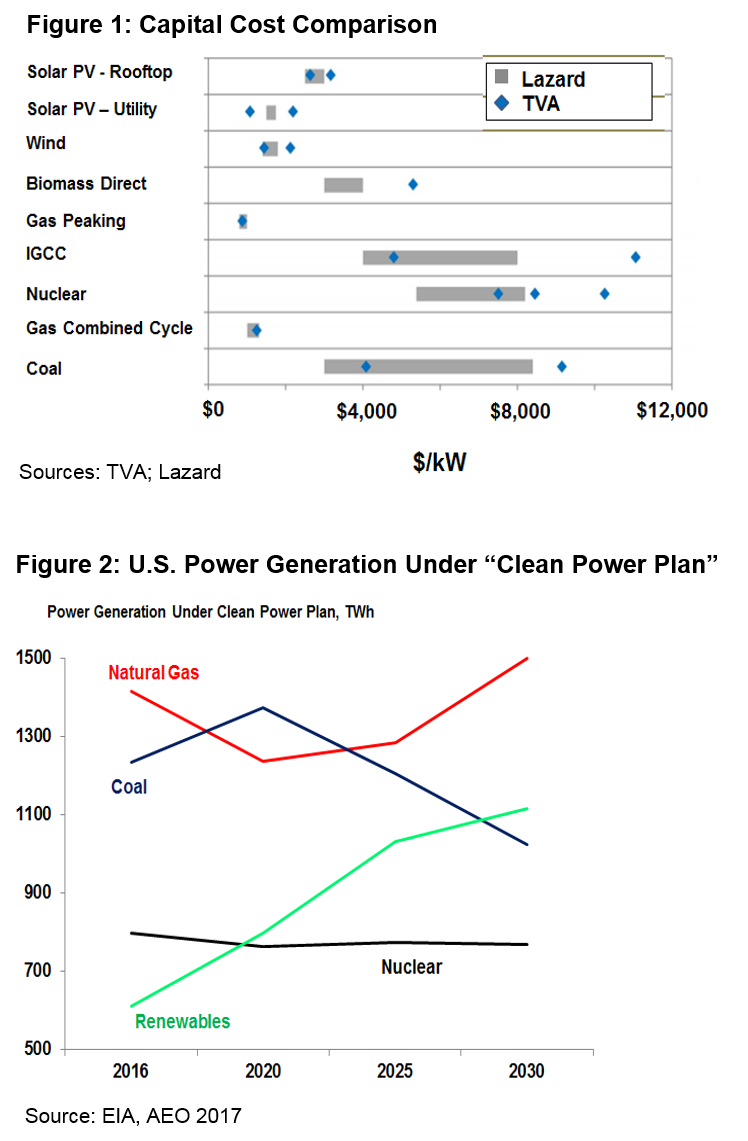

The trend nationally, however, is that more natural gas, wind, and solar generation coupled with increased energy efficiency will be enough to meet new power demand while also reducing emissions. This is especially true because gas prices in 2016 were at their lowest levels since 1999 and costs for solar and wind continue to plummet. For example, since nuclear and solar PV had their first recorded prices in 1956, the cost of nuclear power has gone up by a factor of three, while the cost of solar has dropped by a factor of 2,500. TVA’s assessment of capital costs for various power generation sources generally falls in-line with a highly referenced cost analysis from Lazard’s Levelized Cost of Energy Analysis Version 9.0 (Figure 1). Nuclear remains mostly uncompetitive due to pricing.

Per the Energy Information Administration, there is now about 2,000 MW of utility-scale nuclear set to be retired by 2020, with no capacity additions expected by that time. In contrast, about 10,700 MW of new gas-fired generation and 7,500 of new wind generation are slated to come online. By 2040, about half of U.S. nuclear reactors will be at least 60 years old and could be forced to close.

As a highly reliable, baseload fuel with capacity factors at 90% and above, nuclear power will not be easily replaced. Nuclear “punches above its weight,” actually generating more electricity than its share of capacity would suggest. Thus, nuclear could ultimately play a larger role than is currently being projected (Figure 2).

For example, as non-dispatchable sources of electricity, natural intermittency means renewables are typically only available 20-40% of the time (i.e., why utility-scale storage is so essential for wind and solar to gain market share). And as coal faces pushback because of its higher emissions, a massive capacity build-out and more exports should increase the cost of natural gas.

Additionally, next-generation nuclear technologies like Small Modular Reactors will make nuclear more practical and help to reduce the costs. Importantly, this is in contrast to the emerging key technology for fossil fuels, Carbon Capture and Storage, which is widely accepted as installing higher costs for coal and gas generation.